Last videos

Brazil's trade-war boom

Brazil did not start the world’s newest trade fights. But it may be the clearest beneficiary of them. As tariffs and counter-tariffs rewire supply chains, the global economy is rediscovering a simple truth: when the two largest powers punch each other in the face, the countries that can reliably ship what both sides still need—food, fuel, minerals, and industrial inputs—suddenly gain leverage. In 2026, Brazil sits unusually well-positioned at that crossroads: big enough to matter, diversified enough to pivot, and politically non-aligned enough to sell to almost everyone.The result is a windfall that is not limited to one commodity, one destination, or one trade route. It is an accumulating advantage—built from agricultural dominance, commodity depth, expanding logistics, and a diplomatic posture that often keeps doors open even when superpowers slam theirs shut.The mechanics of a “winner” in a trade warTrade wars rarely “create” demand. They redirect it. When access to a supplier becomes expensive, politically risky, or simply uncertain, buyers don’t stop consuming overnight—they scramble for alternatives. The winners are not necessarily the lowest-cost producers on paper, but those that can scale, deliver consistently, and absorb sudden shifts without breaking contracts or bottlenecking ports. Brazil checks those boxes across multiple categories:- Food and feed: soybeans, corn, meats, sugar, coffee, orange juice, and a rising list of processed foods.- Industrial commodities: iron ore and other mining outputs central to construction, steelmaking, and heavy industry.- Energy and energy-linked products: crude, refined fuels, and biofuels—plus the agricultural inputs that can substitute for constrained supplies elsewhere.In practice, this means Brazil benefits in two distinct ways. First, it captures market share when buyers avoid politically “hot” suppliers. Second, it gains bargaining power on price and contract terms as buyers compete for reliable volumes.The soybean pivot: the clearest example of redirected tradeFew products illustrate the trade-war reshuffle better than soybeans. Soy is not just a food item. It is a strategic input into animal protein, cooking oils, and industrial uses. When tariff retaliation hits agriculture, it hits one of the most politically sensitive sectors in any country—farmers—and it hits fast.In periods of heightened U.S.-China tariff friction, Chinese import demand has repeatedly surged toward Brazil. That shift is not merely a one-off substitution; it can become a structural change if buyers invest in new supply relationships, shipping routines, and processing infrastructure built around Brazilian origin.Once that happens, regaining lost market share becomes difficult even if tariffs later ease. Traders and processors begin to treat the alternative supply line not as a temporary workaround, but as a baseline.Brazil’s advantage here is scale. It can supply massive volumes at competitive costs, and it can expand output over time. Even when weather shocks disrupt harvests, global buyers often still prefer Brazilian origin because the system around it—ports, traders, processors, shipping lanes—has grown used to handling huge flows.Beyond soy: meat, poultry, and the “protein flywheel”Agricultural redirection does not stop at the farm gate. It cascades downstream. When soybean meal becomes abundant and competitively priced, livestock producers can scale. When livestock scales, exports of beef and poultry can rise. When those exports rise, investment flows into cold-chain logistics, feed efficiency, genetics, and processing capacity—further improving competitiveness.This creates a “protein flywheel”: feed drives meat; meat exports justify processing; processing boosts value capture; value capture funds technology and expansion. In a trade-war environment, this flywheel spins faster because importers prioritize resilience over marginal price differences.A quiet shift: from raw supplier to value-added exporterFor decades, Brazil’s critics argued that the country was “stuck” exporting raw materials. The trade-war era complicates that narrative.When supply chains fragment, buyers do not just look for raw inputs. They look for reliable intermediate products: processed foods, refined or semi-processed materials, standardized industrial components, and contract-manufactured outputs that can bypass politically sensitive origins.Brazil has been steadily moving in that direction. Its agribusiness sector, in particular, has expanded processing capacity—crushing soy into meal and oil, scaling meatpacking and poultry processing, and pushing branded and semi-branded exports into more markets.This matters because processed exports typically deliver higher margins, more stable employment, and deeper industrial ecosystems than raw commodity exports. A trade war can act like an accelerant: it rewards producers that can deliver not only bulk volume, but also predictable specifications, traceability, and year-round fulfillment.Playing both sides—without becoming a proxyBrazil’s strategic value in a trade war is not only what it sells, but whom it can sell to. Many countries are forced into binary choices—pick a bloc, pick a standards regime, pick a political camp. Brazil has, so far, avoided being locked into a single side. It trades deeply with China, maintains significant economic ties with the United States, and keeps commercial channels with Europe and large emerging markets.That flexibility is itself a commercial asset. If one destination becomes less attractive—because of tariffs, quotas, sanctions risk, or demand weakness—Brazil can often redirect to another without reinventing its entire export model.This is where the country’s sheer economic breadth becomes decisive. Brazil is not a niche exporter of one resource; it is a multi-commodity, multi-destination supplier with long-established trading relationships. That makes it harder to isolate—and easier to integrate into whatever “re-globalized” world replaces the old one.Tariffs on Brazil can still leave Brazil aheadIt sounds contradictory: how can a country be a “winner” if it is also hit by tariffs? Because relative advantage matters more than absolute pain. If tariffs are applied broadly across many countries, Brazil can still win by being less penalized than competitors—or by benefiting elsewhere from the same tariff regime. Even when Brazil faces targeted duties, the damage depends on how exposed the economy is to the affected market, how easily exporters can pivot, and how many products are exempted or rerouted.In recent tariff episodes, Brazil’s exposure has often been manageable because:- the economy is large and diversified,- exports to any single partner represent only part of total output,- and trade diversion toward other large markets can offset part of the hitIn some scenarios, tariffs even create second-order opportunities: if manufacturers move away from one contested geography, they look for politically safer production bases, raw inputs, and alternative routes. Brazil’s market size, resources, and expanding industrial clusters make it a candidate for that reallocation—especially in resource-linked manufacturing.The critical minerals angle: a new chapter in leverageTrade wars are no longer only about steel, washing machines, or soybeans. They increasingly revolve around the upstream ingredients of modern industry: critical minerals, processing capacity, and the ability to secure supply chains for strategic technologies.Brazil has meaningful reserves in several mineral categories and, crucially, has begun emphasizing the step that matters most: processing and refining, not just digging things out of the ground. In a world where major powers worry about overdependence on any single processing hub, a resource-rich country that can credibly build refining capacity becomes more than a commodity exporter. It becomes a strategic partner.This is a slower-moving advantage than soybeans. Mines and refineries are not built in a season. But the direction is clear: trade conflict is pushing countries to treat supply chains as national-security infrastructure. Brazil, with scale and geological variety, has an opening to become a cornerstone of “de-risked” supply networks—if it can execute.Energy and geopolitics: cheap inputs, tricky politicsTrade wars overlap with sanctions and energy politics, and Brazil has navigated that overlap with a pragmatic streak. In an era of volatile fuel markets, discounted supply offers can lower costs domestically and improve export competitiveness indirectly—because cheaper energy reduces production and logistics costs across the economy. But bargains can come with political risk if suppliers are under sanction pressure or if new restrictions emerge.Brazil’s challenge is to preserve its image as a reliable, rules-respecting trade partner while still protecting domestic economic interests. That balancing act is not unique to Brazil, but it is higher-stakes for a country trying to maximize trade-war gains without triggering punitive responses.Why the momentum is real—and why it is fragileBrazil’s trade-war boom is not an accident. It is a product of structural strengths that the country has spent decades building, even if imperfectly: agricultural technology, large-scale production, export infrastructure, and a commercial diplomacy that generally seeks options rather than ultimatums. But the boom is also fragile, for three reasons.1) Infrastructure is still the bottleneck. Brazil can grow more soy, raise more cattle, and mine more ore—but if roads, rail, ports, and storage cannot keep up, the advantage erodes into delays and higher costs. Global buyers reward reliability; a single season of congestion can push them to diversify elsewhere.2) Environmental constraints are tightening. The world is not only watching prices. It is watching land use, deforestation, and traceability. Markets and regulators increasingly demand proof of compliance. Brazil’s export future depends on whether it can scale production while convincingly controlling illegal deforestation and improving transparency across supply chains. Without that, access to premium markets can narrow.3) Trade wars shift quickly—and can turn inward. A country can benefit from diversion today and be targeted tomorrow. If Brazil’s gains become politically salient abroad—especially in election cycles—calls for countermeasures can rise. The “winner” label can paint a target.The bigger picture: Brazil as a stability premiumUltimately, Brazil’s biggest advantage in a fractured global economy may be intangible: it sells stability. Not perfection—Brazil remains a complex, high-variance country with fiscal pressures, political noise, and real governance challenges. But compared with flashpoint suppliers, it offers something increasingly scarce: the ability to ship essential goods at scale while maintaining working relationships across rival blocs.In a world where trade is becoming a tool of statecraft, that ability is worth a premium. And that is why Brazil can emerge as the big winner of the trade war—not because it avoids the fallout, but because it is structurally built to capture the rerouting, the repricing, and the reinvestment that follow when global trade stops being “efficient” and starts being “strategic.”

Poland trusts only hard Power

On Europe’s exposed north‑eastern flank, Poland is recasting its security doctrine around a stark premise: deterrence rests on hard power that is visible, ready and overwhelmingly national. Alliances still matter in Warsaw, but the country’s leaders are behaving as if, in the final analysis, neither Brussels nor Washington can be relied upon to act as swiftly—or as single‑mindedly—as Polish interests might require.At the heart of this shift is an unprecedented build‑up of fixed and mobile defences on the frontier with Belarus and Russia’s Kaliningrad exclave. The multi‑year East Shield programme, announced in 2024 and now well under way, blends traditional fortifications and obstacles with modern surveillance, electronic warfare and rapid‑reaction infrastructure along the entire eastern border. In mid‑2025, authorities confirmed the addition of minefields to parts of the project, underscoring a move from symbolic fencing towards denial‑by‑engineering designed to slow and channel any hostile incursion long enough for Polish artillery, air defence and ground forces to engage.This is not theory. Over the past 18 months, Polish airspace has been violated by Russian missiles and, most recently, waves of drones transiting from Belarus. In September 2025, Polish and allied aircraft shot down intruding drones—widely noted as the first kinetic engagement inside NATO territory linked to the war on Ukraine. Warsaw temporarily closed crossings with Belarus during Russia‑led military exercises and then reopened them once the drills ended, a sign of a government calibrating economic realities against a more volatile air‑and‑border threat picture. The message, repeated in official statements, is that incursions will be met with force when they are “clear‑cut” violations.The second pillar of Poland’s doctrine is money—lots of it. Poland now spends the highest share of GDP on defence in the Alliance, around the mid‑4% range in 2025, with plans signalled to push towards the high‑4s in 2026. That places Warsaw well beyond NATO’s post‑Hague summit ambition of substantially increasing “core defence” outlays across the Alliance in the coming decade. Crucially, a larger slice of Poland’s budget goes to kit rather than salaries: air‑and‑missile defences, long‑range fires, armour, and the infrastructure to sustain them.Procurement lists read like an order‑of‑battle overhaul. Deliveries of Abrams tanks from the United States are ongoing, alongside large tranches of K2 tanks and K9 self‑propelled howitzers from South Korea, with a follow‑on K2 order establishing long‑term assembly and manufacturing in Poland. The first Polish F‑35s are in training pipelines with in‑country deliveries scheduled to begin next year, while the Aegis Ashore ballistic‑missile defence site at Redzikowo has been declared operational and integrated into NATO’s shield. The permanent U.S. V Corps (Forward) headquarters in Poznań and a standing U.S. Army garrison in Poland anchor allied command‑and‑control on the Vistula. Yet, strikingly, Warsaw is not content to import its way to security; it is racing to on‑shore the industrial sinews of war, pouring billions of złoty into domestic production of 155 mm artillery shells and selecting foreign partners to build new ammunition plants that can feed both Polish units and European supply lines.Manpower policy is being re‑engineered with equal ambition. The government has set out plans to make large‑scale, publicly accessible military training available—ultimately to every adult male—while expanding volunteer pathways and aiming to train 100,000 people annually by 2027. This push complements growth targets for the active force and reserves, all intended to ensure that Poland can surge trained personnel quickly if the strategic weather turns.Where does Brussels fit into this? Relations have thawed on rule‑of‑law disputes, unlocking access to long‑delayed EU funds. But Warsaw has made plain it will not implement elements of the EU’s new migration pact that would compel acceptance of relocated migrants; it has also reintroduced temporary border checks with Germany and Lithuania, citing organised crime and irregular migration. On the security side, Poland is an enthusiastic driver of the emerging “drone wall” concept along the EU’s eastern frontier. Taken together, these choices sketch a posture of selective integration: take European money when it aligns with national priorities, but reserve sovereign latitude on borders and internal security.Nor is the reliance on force simply a European story. Across the Atlantic, U.S. signals have been mixed in recent years—from remarks that appeared to cast doubt on automatic protection for “delinquent” NATO members, to renewed assurances in 2025 that American troops will remain in Poland and might even increase. Polish officials welcome tangible U.S. deployments and capabilities, but they are plainly hedging against political oscillation in Washington by accelerating self‑reliance in their defence industry, stockpiles and training base. The governing logic is straightforward: alliances deter best when the ally in harm’s way can fight immediately and hold ground.Domestic politics amplify this course. The election of Karol Nawrocki as president in August 2025 has added a sovereigntist accent to Warsaw’s foreign‑policy soundtrack. In his inaugural framing, Poland is “in the EU” but will not be “of” the EU in any way that dilutes competences crucial to national security and identity. That stance intersects with hard security in one especially consequential area: mines. Alongside the Baltic states, Poland announced its intention in 2025 to withdraw from the Ottawa (anti‑personnel mine) treaty, arguing that Russia’s conduct and the geography of the Suwałki corridor demand maximum defensive optionality. Humanitarian advocates warn of the risks; the government replies that modern doctrine, marking and command arrangements can mitigate them.All of this costs money—and fiscal stress is visible. Ratings agencies have flagged high deficits and debt dynamics, shaped in part by defence outlays. Warsaw recently chose to trim the loan component of its EU recovery‑fund package, prioritising grants as deadlines loom. The balancing act is delicate: sustain deterrence at scale while keeping public finances credible and an economy already carrying the weight of war‑time disruptions competitive.Yet step back from the line items, and a coherent doctrine comes into view. Poland is not repudiating its alliances; it is re‑weighting the bargain. The country is building a fortified frontier and a war‑capable society on the assumption that credible force—owned, stationed and manufactured at home—will decide what happens in the first hours and days of any crisis. If Brussels and Washington arrive with reinforcements, all the better. But the governing bet in Warsaw is brutally simple: only hard power keeps the peace on the Bug and the Vistula.

Cuba's hunger Crisis deepens

Cuba’s food emergency has sharpened into a pervasive hunger crisis. Queues for basic staples lengthen; subsidised rations arrive late or shrunken; prolonged black‑outs spoil what little families can buy. At the centre sits a long‑running question of policy as well as morality: should the United States lift—wholly or in part—its embargo?What is driving hunger?Cuba’s economy has been in a grinding downturn since 2020, with a steep loss of foreign currency, collapsing agricultural output and a power grid plagued by breakdowns. The island imports most of what it eats; when hard currency runs short, shipments of wheat, rice, oil and powdered milk stall. Ration books still guarantee a monthly “basic basket”, but the contents are smaller and more erratic than before. Long electricity cuts—now at times island‑wide—destroy refrigerated food and disrupt mills, bakeries and water systems. In March 2024, rare public protests erupted over black‑outs and empty shops; since then, outages and shortages have persisted well into 2025.Behind the empty shelves lies a structural farm crisis. Sugar—once the backbone of the economy—has withered to a fraction of historic output, starved of fuel, fertiliser, parts and investment. Cane shortfalls ripple into food, transport and export earnings. Livestock herds have thinned, and diesel scarcity makes planting and distribution harder. Even when harvests occur, logistics failures and power cuts mean produce rots before reaching markets.How far does the embargo matter?Two facts can be true at once. First, Cuba’s own policy choices—tight state controls, delayed reforms, pricing distortions and a faltering energy system—are central to the crisis. Second, U.S. sanctions amplify the shock. The embargo, codified in U.S. law, restricts trade and finance with Cuba’s state sector and deters banks and insurers from handling even otherwise lawful transactions. Although food and medicine are formally exempt, Cuba must typically pay cash in advance and cannot access normal commercial credit from U.S. institutions; compliance risk pushes up costs, slows payments and scares off shippers and intermediaries. Cuba’s continued designation as a “State Sponsor of Terrorism” further chills banking ties. In short: exemptions exist on paper, frictions mount in practice.There are countervailing trends. Since 2021, Havana has allowed thousands of private micro‑, small‑ and medium‑sized enterprises (MSMEs) to operate; many import food and essentials the state cannot supply. In 2024, Washington moved to let independent Cuban entrepreneurs open and use U.S. bank accounts remotely and to widen authorisations for internet‑based services and payments. Yet the political pendulum has swung back toward greater sanctions in 2025, and Cuba’s own tighter rules on the private sector have added uncertainty. The net effect is an ecosystem still too fragile to steady food supplies.Is this a “famine”?No international body has declared a technical famine in Cuba. That term has a high evidentiary threshold. But food insecurity is severe and widespread: calorie gaps, ration cuts, milk shortages for young children and recurrent bakery stoppages paint a picture of a humanitarian emergency in all but name. Global agencies have stepped in to help secure powdered milk and other basics; even so, distribution delays and funding shortfalls mean stop‑start relief.Should the United States lift the embargo?The humanitarian case is powerful. Lifting or substantially easing the embargo would lower transaction costs, restore access to trade finance, reduce shipping and insurance frictions, and widen suppliers’ appetite to sell. That would not, by itself, fix Cuba’s domestic constraints, but it would remove external bottlenecks that particularly harm food imports, farm inputs and power‑sector maintenance. In a context of ration cuts and soaring prices, fewer frictions mean more staples on plates.The governance caveat is equally real. Sanctions were designed to press for pluralism and human rights; critics fear that broad relief could entrench a state‑dominated economy with poor accountability, and that aid or hard currency could be diverted. Nor is a full lift simple: the embargo is written into statute and requires congressional action. In U.S. domestic politics, that bar is high.A pragmatic path throughGiven legal and political realities, three steps stand out as both feasible and fast‑acting:1) Create a humanitarian finance channel for food and farm inputs. Authorise insured letters of credit and trade finance for transactions involving staple foods, seeds, fertiliser, spare parts for milling, cold‑chain equipment and water treatment—available to private MSMEs and non‑sanctioned public distributors alike, with end‑use auditing.2) De‑risk payments for independent Cuban businesses. Lock in and broaden 2024 measures allowing Cuban private entrepreneurs to hold and use U.S. bank accounts remotely, and permit “U‑turn” transfers that clear in U.S. dollars when neither buyer nor seller is a sanctioned party. Pair this with enhanced due diligence to prevent diversion.3) Protect the food pipeline from energy failures. License sales of critical spares and services for power plants and grid stability that directly safeguard bakeries, cold storage, water pumping and hospitals. Where necessary, allow time‑bound fuel swaps for food distribution fleets under third‑party monitoring.Alongside U.S. actions, Cuba must do its part: secure property rights for farmers, ensure price signals that reward production, remove import monopolies that choke private wholesalers, cut administrative hurdles for MSMEs, and prioritise grid repairs that keep food systems running. Without these domestic adjustments, external relief will leak away in lost output and waste.The bottom lineCuba’s hunger crisis is the product of compounding internal and external failures. Ending or meaningfully easing U.S. sanctions on food, finance and energy‑for‑food lifelines would save time, money and calories; it is defensible on humanitarian grounds and achievable through executive licensing even if Congress leaves the core embargo intact. But durability demands reciprocity: Havana must unlock farm productivity and private distribution, and Washington should target relief where it most directly feeds Cuban households. Starvation risks are non‑ideological. Policy should be, too.

Terrorist state Iran attacks Israel with missiles

Iran has attacked Israel with ballistic missiles. The skies were filled with deadly missiles fired by the criminal mullah regime at the Jewish state. The Iranian terrorist regime has fired a total of 181 missiles at Israel. According to information, there have been impacts in several Israeli cities, including Tel Aviv.

Lebanon: Is a new wave of refugees coming to the EU?

A representative for the UN's refugee agency told Euronews that Europe could be seen as a refuge amid fears of a growing humanitarian catastrophe in the Middle East, prompted by the conflict between Israel, Iran, Lebanon and Hamas.

Ukraine: Zelenskyy appeals for international aid

Ukrainian President met with several entities on Wednesday to discuss strengthening Ukraine's defence, as well as securing aid in preparation for the winter.

EU vs. Hungary: Lawsuit over ‘national sovereignty’ law

Brussels has stepped up its legal action against Hungary's "national sovereignty law," arguing it violates a wide range of fundamental rights.

Vladimir Putin, War criminal and Dictator of Russia

Putin critic Vladimir Kara-Mursa was one of eight Russian dissidents released in the largest international prisoner exchange since the Cold War. He says he thought he would be executed the day he was taken out of his cell.This is just one story related to the nefarious mass murderer and anti-social war criminal, Russian dictator Vladimir Putin, 72.

Electric car crisis: Future of a Audi plant?

Audi's Brussels plant is assembling an 80,000 euro electric SUV, which turns out to be too expensive for Europeans. After 2025, production will probably relocate to Mexico. Workers and unions are not happy.

Zelenskyy: ‘What worked in Israel work also in Ukraine’

If missile defence was possible for Israel against the terrorist state of Iran, missile defence must also be made possible for Ukraine against the terrorist state of Russia!Rutte vowed when he took office on Tuesday to help shore up Western support for Ukraine, which has been fighting Russia’s full-scale invasion since February 2022.

EU: Tariffs on all Chinese electric Cars

Chinese producers of electric vehicles will soon face steep tariffs before selling their high-end goods in the EU market.

Iran lifts Dollar, sinks Euro

To say the dollar is crushing the euro sounds like tabloid economics. Yet the first full geopolitical stress test of 2026 has produced exactly the directional result implied by that phrase. Money is again flooding toward the U.S. currency while the euro is being repriced against a harsher reality: Europe remains more vulnerable to imported energy shocks, trade disruption and slower growth than the United States.By the end of the first week of March, EUR/USD was trading around 1.16, the dollar index was back near 99, and oil had surged above $90 a barrel as traders priced a wider Middle East disruption. That is not a historic collapse of the single currency. It is, however, a decisive reminder of how quickly markets still fall back into the old hierarchy when fear becomes the dominant force.Iran is central to that hierarchy test, not because its economy sets the global reserve system, but because it sits at the junction where sanctions, energy flows, shipping lanes and regional war all collide. Internally, the country has been living through a severe monetary breakdown. The rial plunged to roughly 1.5 million to the dollar earlier this year, protests erupted, and the state’s response deepened the atmosphere of repression and uncertainty. Externally, every escalation connected to Iran forces markets to reprice the cost of moving oil, gas, cargo and capital.The Strait of Hormuz is the critical mechanism. Roughly 20 million barrels a day of oil and about a fifth of global LNG trade move through that narrow channel. Any threat there instantly travels through crude contracts, gas benchmarks, marine insurance, tanker availability and inflation expectations. Europe does not have to be the largest direct buyer of Hormuz crude to be hit hard. It is enough that Europe is the more energy-sensitive, more import-dependent, and more politically fragmented economic bloc.That vulnerability is now colliding with a euro area that was improving, but still far from robust. Inflation in February edged back up to 1.9 percent. Output in the fourth quarter of 2025 rose just 0.2 percent. The ECB’s own baseline for 2026 is growth of 1.2 percent. Those are not the numbers of an economy built to absorb a prolonged external energy shock without political or financial strain. If fuel, gas and freight costs remain elevated, the euro area is pushed back toward the policy trap that haunted it after 2022: softer activity, stickier prices, and a currency market that demands a discount for both.The logistics channel makes the shock even broader than the oil story suggests. Trade between Asia, the Gulf and Europe is already being rerouted or repriced. Airfreight costs on Asia-Europe lanes have jumped sharply. Shipping delays, war-risk premiums and booking suspensions are beginning to feed through supply chains. That matters for Europe because the euro is not merely a currency. It is the price label attached to an industrial and consumer economy that still depends on long, vulnerable trade arteries.The United States is not immune. Higher oil prices, tighter freight and nervous markets will still hit American households and businesses. But the U.S. enters this episode with a different energy position, deeper domestic capital markets and a far greater capacity to attract crisis money. In other words, the same shock that raises inflation risk can also increase demand for the currency in which that shock is being hedged. That is a privilege the euro still does not fully share.This is why the phrase “monetary order” is not exaggerated. The international order is not defined only by speeches about multipolarity or by occasional non-dollar trade settlements. It is defined by what investors, banks, commodity traders, insurers and central banks actually do when a geopolitical shock threatens liquidity. They reach for the currency that dominates settlement, collateral, sovereign debt markets and emergency funding. They reach for the dollar.Even the reserve data tells a more sober story than the rhetoric around de-dollarization. Diversification is real, but it remains gradual rather than revolutionary. In the latest IMF reserve snapshot for 2025’s second quarter, the dollar still accounted for 56.32 percent of allocated foreign-exchange reserves. The euro stood at 21.13 percent. That is a meaningful role for the single currency, but it is not monetary parity. And when a live geopolitical shock erupts on the edge of the world’s most important energy corridor, that gap becomes political as well as financial.Iran’s turmoil sharpens the lesson. A collapsing currency is not just an economic symptom. It is a measure of shrinking state credibility. The more households and firms in Iran think in dollars, gold or foreign stores of value, the less authority the rial has as a unit of account, a store of value and a symbol of sovereignty. Sanctions then do more than cut revenue; they tighten the external constraints around a country whose domestic money is already losing legitimacy. That is why chaos in Iran can radiate into the wider monetary system without Iran ever becoming a reserve-currency power itself.There is also a strategic irony here. For years, the most confident forecasts of a post-dollar world assumed that repeated sanctions, geopolitical fragmentation and alternative payment channels would steadily weaken America’s monetary primacy. Yet in the current crisis, the opposite short-term effect has emerged. The harsher the fear, the more the market reverts to dollar behavior. That does not invalidate the long debate over a more multipolar currency future. It simply proves that the future has not arrived yet.For Europe, the conclusion is uncomfortable but unavoidable. The euro cannot become a true equal to the dollar on institutional elegance alone. It needs faster and more durable growth, deeper capital markets, more unified fiscal capacity, and an energy system that is far less exposed to external shocks. Until those foundations are stronger, every major geopolitical disruption will tell the same story: the dollar gathers panic, the euro absorbs vulnerability.For markets, the next chapter depends on duration. If the conflict is contained, shipping stabilizes and energy infrastructure avoids further damage, part of the dollar’s new crisis premium can evaporate. But if Hormuz remains constrained, if Gulf export capacity is knocked back further, or if sanctions and retaliation intensify, the euro will face a far tougher test. In that world, a move toward much lower euro levels would stop being a speculative talking point and start becoming the working assumption of 2026.So the slogan is dramatic, but the underlying verdict is real. The dollar is not obliterating the euro. It is, however, beating it decisively in the one contest that still defines the system when panic strikes: the market’s instantaneous vote on which currency can carry fear. Chaos in Iran has not created a new monetary order. It has exposed, with uncomfortable clarity, how much of the old one still survives.

Hormuz Shock Risk rising

In the narrow waters between Iran and Oman, the world’s most important energy choke point has turned into the epicenter of a fast-moving economic threat. What began as a military escalation has morphed into something markets fear even more: a sustained disruption of maritime traffic through the Strait of Hormuz—an artery that, in normal times, carries a staggering share of global oil and liquefied natural gas flows.Over just days, the strait’s risk profile has shifted from “tense” to “near-uninsurable.” Commercial ship operators have slowed, paused, or rerouted voyages. Tankers have clustered in holding patterns. War-risk premiums have jumped. Freight rates have surged. For energy importers and manufacturers far from the Gulf, the shock is already spreading through prices, delivery schedules, and financial expectations.The question is no longer whether the world can absorb “higher oil for a week.” The question is whether the world is about to relearn a harsher lesson: when Hormuz is threatened, the global economy doesn’t just pay more—it changes behavior, and that behavioral shift can snowball into a broader, longer-lasting disruption.Why the Strait of Hormuz matters more than any headlineThe Strait of Hormuz is not merely a strategic symbol; it is an economic switchboard. A significant portion of the world’s seaborne crude oil and petroleum products transits these waters, alongside a major share of global LNG shipments. Even brief interruptions can tighten supply immediately because many refineries and power systems are designed around steady inflows, not sudden reroutes or prolonged delays.Yes, some producers have partial bypass options—pipelines that move oil to ports outside the Gulf—but those alternatives are limited and cannot replicate the strait’s full capacity at short notice. That structural bottleneck is why any serious threat to freedom of navigation in Hormuz instantly becomes a global pricing event.What “attacking Hormuz” looks like in practiceA disruption does not require a formally declared blockade. It can be achieved through a blend of tactics that make commercial passage too dangerous or too expensive:- Direct strikes or attempted strikes on vessels near the transit corridor.- Drone and missile pressure that forces ships to switch off tracking, scatter, or delay.- Threats against shipping that deter crews, owners, and charterers.- Mine-laying risk—even the suspicion of mines can freeze traffic, because clearing operations are slow and technically demanding.- Targeting port and coastal infrastructure in the wider region, creating downstream bottlenecks even if some vessels still attempt passage.In the shipping world, perception becomes reality. If underwriters cannot price risk with confidence, coverage is withdrawn or priced so high that voyages become uneconomic. When insurers step back, lenders, charterers, and operators follow—often within hours.The immediate market mechanics: from fear to scarcityEnergy markets move on marginal barrels and marginal cargoes. When a major corridor is disrupted:1. Spot prices react first. Traders price in expected shortages and scramble for alternatives.2. Physical cargoes re-route or stall. That introduces real scarcity, not just financial speculation.3. Refiners bid more aggressively for replacements. The same barrels get chased by more buyers.4. Storage and strategic reserves become bargaining chips. Governments consider releases; companies hoard.5. Volatility becomes the product. Uncertainty lifts option premiums and hedging costs, which feed back into consumer prices.Even countries that do not buy Gulf oil directly still feel the impact because oil is globally priced and globally substituted. If one region’s supply tightens, another region’s barrels get pulled toward the highest bidder. The result is a synchronized, worldwide repricing.The second-order shock: LNG, power prices, and industrial stressOil grabs headlines, but LNG often delivers the sharper economic pain. Gas markets are increasingly global, yet still constrained by liquefaction capacity, shipping availability, and terminal infrastructure. When LNG cargoes are delayed, power utilities and large industrial users face immediate dilemmas:- pay extreme spot prices,- switch fuels (where possible),- curtail operations,- or pass costs through to households and businesses.Energy-intensive sectors—chemicals, fertilizers, metals, cement, and some food processing—can experience sudden margin collapse. That’s how an energy shock migrates into inflation, employment pressure, and weaker growth.Shipping and supply chains: the hidden multiplierA Hormuz disruption is not only an “energy story.” It is a logistics story with compounding effects.If carriers divert around longer routes, costs rise through:- extra fuel burn,- longer transit times,- crew and vessel utilization strain,- congestion at alternative hubs,- and surcharges for security, insurance, and war risk.Those delays hit everything: components, pharmaceuticals, electronics, industrial inputs, and consumer goods. Businesses that operate “just-in-time” inventories suffer first; small suppliers and retailers often suffer hardest because they lack bargaining power and buffer stock. In modern supply chains, time is money—and disruption is inflation.The inflation problem: central banks get boxed inA severe Hormuz shock creates a policy nightmare. Higher energy and transport costs push inflation up, while uncertainty and curtailed demand push growth down. That mix can resemble “stagflationary” conditions, where:- consumers face higher bills,- companies face higher costs,- investment slows due to uncertainty,- and central banks struggle to choose between fighting inflation or supporting growth.Even if the initial spike fades, the volatility itself can keep inflation expectations elevated—especially if businesses begin building “risk premiums” into pricing and wage negotiations.Financial markets: stress travels faster than oilMarkets do not need months to react. They reprice risk instantly:- Energy and defense assets can surge.- Airlines, logistics, and heavy industry can come under pressure.- Emerging markets that import energy may see currency weakness and higher financing costs.- Credit spreads can widen if investors fear recession or persistent inflation.A key vulnerability is the intersection of energy prices and debt. Many governments and companies refinanced during periods of lower rates and calmer conditions. If energy-driven inflation keeps rates higher for longer, or if recession risks rise, debt sustainability questions re-emerge—especially for import-dependent economies.Who is most exposed?Exposure is not purely geographic. It is structural.- Major Asian importers are highly sensitive due to scale and reliance on seaborne energy.- Energy-poor economies with limited strategic reserves feel price spikes fastest.- Industrial exporters suffer when input costs rise and shipping slows.- Low-income households face the harshest real-world impact as energy and food costs rise.Food becomes a late-stage amplifier: energy prices raise fertilizer and transport costs, which can filter into agricultural pricing cycles and, eventually, consumer food inflation.Can the shock be contained?There are stabilizers, but none are perfect.1) Naval protection and convoying Escorts can reduce some risks, but they cannot eliminate them—especially if threats are asymmetric (drones, missiles, mines). A single successful strike can trigger a renewed insurance retreat.2) Strategic reserves Reserves can smooth short-term supply gaps and signal policy resolve. But they are a bridge, not a solution, if disruption persists.3) Bypass infrastructure Pipelines and alternative ports help, yet capacity is limited and subject to its own vulnerabilities.4) Demand response High prices can reduce demand, but that “solution” often arrives through economic pain—slower growth and weaker consumption.The most effective stabilizer is political: de-escalation that restores predictable navigation. Without it, markets will keep pricing risk, and supply chains will keep adapting in more expensive ways.Are we on the brink of a global economic shock?If disruption remains brief and contained, the world may endure a sharp but temporary price spike. But if attacks continue, if insurers and carriers remain unwilling to operate normally, or if the threat environment evolves into mine warfare or persistent strikes, the risk shifts decisively toward a broader shock.The dangerous feature of a Hormuz crisis is not only the initial damage—it is the feedback loop: higher risk → fewer ships → tighter supply → higher prices → more panic buying and hoarding → further tightening.Once that loop takes hold, reversing it requires more than statements and short-term fixes. It requires restored confidence—commercial, military, and political—that the corridor can function safely again. For now, the world is watching a narrow strip of water where economics and security collide. The longer that collision continues, the more likely it is that what looks like a regional conflict becomes a global cost-of-living event.

How Swiss Stocks tamed Prices

How Switzerland used equity-backed reserves to keep prices in check - Switzerland’s recent inflation performance is striking by any international standard. While much of the developed world grappled with price rises far above target, Swiss consumer-price inflation has been brought back to muted rates and, at times, hovered close to zero. The country did not stumble upon a miracle cure. Rather, it relied on an institutional playbook that blends a credible inflation target, a strong and freely moving currency—and, crucially, a uniquely structured central‑bank balance sheet in which roughly a quarter of foreign‑exchange reserves is invested in global equities.At the heart of the Swiss approach lies the exchange‑rate channel. For more than a decade the Swiss National Bank (SNB) accumulated very large foreign‑currency reserves to manage excessive upward pressure on the franc. Those reserves are diversified across currencies and asset classes, with a deliberately significant allocation to equities managed on a passive, market‑neutral basis. Building a portfolio that earns an equity risk premium over time was not an end in itself; it was a way to improve the risk‑return profile of the reserves while maintaining ample firepower for currency operations.That firepower proved pivotal when global energy and goods prices surged. In 2022 and 2023 the SNB shifted stance and used its reserves in the opposite direction—selling foreign currency to allow a measured appreciation of the franc. A stronger franc lowers the local‑currency price of imported goods and services, damping inflation via “imported disinflation”. Because the reserves had been amassed in earlier years, and because a sizeable slice was in equities that tended to deliver solid returns over time, the central bank could act decisively without jeopardising balance‑sheet resilience.The portfolio structure also matters for confidence. An equity share—held broadly across markets and sectors, with exclusions on ethical grounds and with no investments in Swiss companies—signals that the reserves are not a dormant hoard but a well‑diversified buffer aligned with long‑run value preservation. When equity markets rose strongly in 2024, gains on those holdings (alongside gold and currency effects) replenished the central bank’s financial buffers. That, in turn, reinforced the credibility of policy at precisely the moment when keeping inflation expectations anchored was most important.None of this should be mistaken for the SNB “using the stock market” as its primary inflation tool. Monetary policy still rests on an explicit price‑stability objective, a conditional inflation forecast and the policy rate. Indeed, as inflation returned to the target range, the policy rate could be reduced again in 2024–2025. But the equity‑backed reserves shaped the backdrop: they made it easier to tighten monetary conditions through the exchange rate when prices were accelerating, and they underpinned confidence in subsequent easing once inflation receded.Switzerland’s low and recently near‑zero inflation cannot be ascribed to reserves alone. The country’s energy mix and regulated price components dampened the direct pass‑through from global fuel shocks; the consumption basket assigns a smaller weight to energy than in many peers; and the franc’s safe‑haven status consistently mutes imported price pressures. What distinguishes the Swiss case is how these structural features were complemented by an ample, well‑diversified reserve portfolio—including global equities—that allowed timely foreign‑exchange operations without calling market confidence into question.The lesson is not that every central bank should load up on shares. Institutional mandates, legal frameworks, market depth and exchange‑rate regimes differ widely. Rather, Switzerland shows that, for a small open economy with a safe‑haven currency, a disciplined, transparent reserve strategy—one that tolerates equity exposure while avoiding conflicts of interest at home—can support the nimble use of the exchange‑rate channel. In the inflation shock of recent years, that combination helped bring prices back under control.As of late summer 2025, Switzerland’s inflation remains subdued and close to the midpoint of its price‑stability range. The franc is firm, policy is data‑driven, and the central bank’s balance sheet—anchored by highly liquid bonds and a passive equity allocation—retains the flexibility to lean against renewed price pressures or, if conditions warrant, to cushion the economy. Switzerland did not “magic away” inflation by buying shares; it designed a balance sheet that could do its day job when it mattered.

Israel presses Tehran

By March 8, 2026, Israel’s campaign against Iran no longer looks like a tightly bounded military operation designed merely to restore deterrence. It now appears to be something broader, harsher, and more politically ambitious: an effort to keep striking until the Islamic Republic can no longer function with strategic coherence, political confidence, or an orderly chain of succession.What began with attacks on military, leadership, and nuclear-related targets has moved steadily closer to the core machinery of power. The shift is unmistakable. Israel is not only trying to degrade missiles, commanders, and command networks. It is also bearing down on the institutions that allow clerical rule to intimidate society, absorb shocks, and recover after crisis. The logic is brutal but clear: a regime can survive heavy battlefield damage if its internal organs of coercion and succession remain intact. Once those organs begin to fracture, however, a military campaign starts to bleed into a political one.That is why the death of Ali Khamenei changed the meaning of the war. Removing the supreme leader did not simply decapitate the man at the top of the system. It forced Iran into the most sensitive test the Islamic Republic can face in wartime: whether it can reproduce legitimacy and authority fast enough to prevent elite panic, institutional rivalry, and public defiance. In ordinary times, succession in Iran is opaque by design. In wartime, under bombardment, opacity becomes weakness. Uncertainty multiplies. Rumor becomes strategy. Every delay in producing a stable successor creates space for fear, hedging, and internal competition.Iran may still move quickly to formalize a new supreme leader. Reports now indicate that the body responsible for choosing the next leader has reached a decision, even if the identity of that choice has not yet been officially unveiled. But speed is not the same as stability. A successor selected under bombardment, under threat, and under suspicion of outside manipulation would inherit authority under siege from the first moment. In practical terms, that means the regime is trying to project continuity while the ground beneath it is still shaking.Israel seems determined to exploit exactly that vulnerability. Its public rhetoric has become far more explicit than the old language of deterrence or preemption. Israeli leaders are no longer speaking only about removing immediate threats. They are openly describing a war that could create the conditions in which Iranians themselves bring down the system. That matters because language follows intent. States do not repeatedly invoke the possibility of internal collapse unless they believe the battlefield and the political arena are beginning to merge.The strategic logic now visible is that Israel is not preparing to stop at symbolic punishment. It is pressing forward with a theory of victory that blends military attrition, leadership decapitation, succession chaos, and pressure on internal repression. In that framework, air power is not meant to conquer Iran in any conventional sense. It is meant to hollow out the regime’s ability to command, to frighten, and to replace itself.Seen through that lens, Israel’s widening target selection makes grim sense. Strikes against organs of internal security are about more than military efficiency. They are about weakening the very structures that monitored dissidents, suppressed protest movements, enforced fear, and kept the streets manageable whenever public anger surged. Attacks on fuel depots and energy infrastructure serve a parallel purpose. They do not merely increase the cost of war for Tehran; they test the state’s ability to preserve daily life in the capital. A regime that cannot keep fuel flowing, smoke off the skyline, and basic confidence intact starts to look less like an enduring order and more like a system under slow liquidation.Israel also appears to believe that this moment is unusually favorable because the war is landing on top of a pre-existing domestic crisis. Iran was already under severe internal strain before the latest wave of strikes. The economy had been battered by sanctions, currency collapse, inflation, shortages, blackouts, and chronic water stress. Public anger had already spilled into the streets. What makes the present moment especially dangerous for Tehran is not only that people are exhausted, but that the base of discontent has widened. Social exhaustion, merchant unrest, student anger, and the steady erosion of economic confidence can be managed one by one. When they begin to overlap, authoritarian systems stop looking immovable.That social dimension matters enormously. Governments can often suppress unrest when it is confined to students, activists, or a single urban class. It becomes more serious when discontent reaches people who usually prefer order to upheaval: traders, families worried about food prices, workers struggling with shortages, and citizens who may not share the same ideology but do share the same exhaustion. A regime loses more than popularity when that happens. It loses the sense that daily life, however difficult, still has a workable center.Yet collapse is not automatic. Regimes built on fear, patronage, and force often survive far longer than outside observers expect. Iran’s system still retains organized coercive power, ideological loyalists, and a security culture that was built precisely to withstand moments like this. The Revolutionary Guard remains the most decisive institution in the country, and history offers no guarantee that pressure from the air will produce a democratic opening on the ground. There is an equally serious possibility that the opposite could happen: that a weakened clerical order gives way not to pluralism, but to a more nakedly militarized state dominated by hardline security factions.That is one of the central uncertainties now hanging over the succession. Iran’s constitutional framework provides a temporary leadership mechanism and assigns the task of choosing a new supreme leader to the clerical establishment. In theory, that offers continuity. In practice, continuity is exactly what Israel appears unwilling to allow. By signaling that any successor who preserves the same strategic line could also become a target, Israel is turning succession itself into a battlefield. The aim, in effect, is not merely to kill a leader, but to break the regime’s confidence that leadership can be regenerated at all.This is a profound shift. Deterrence usually works by threatening pain if an adversary acts. What is emerging here looks closer to regime denial: the effort to convince Tehran that it may no longer be able to maintain a functioning model of rule. Once that threshold is crossed, the question is no longer only whether Iran can retaliate. It is whether Iran can still govern.That is why the phrase “Israel won’t let up” should now be taken literally. From Jerusalem’s perspective, stopping too soon may be more dangerous than continuing. A paused campaign could leave a bruised but surviving regime determined to rebuild, rearm, and retaliate with even greater urgency. An incomplete victory would allow Tehran to present survival itself as triumph, purge internal hesitation, and return later with a sharper sense of strategic revenge. For Israeli decision-makers, the conclusion seems to be that if the Islamic Republic remains intact at the center, then even serious battlefield damage may prove temporary.Yet the costs of pursuing this logic are already immense and rising. The war has produced a mounting civilian death toll inside Iran, severe damage across several fronts, toxic smoke over Tehran, regional strikes on critical infrastructure, and expanding instability far beyond the immediate battlefield. Lebanon is bleeding again. Gulf states are being dragged deeper into the conflict. Energy markets are on edge. What began as a direct confrontation has become a region-wide stress test of state resilience, civilian endurance, and international restraint.Nor is there any clean political endgame in sight. Even if Israel succeeds in pushing the clerical system toward fracture, what comes next remains deeply uncertain. A public uprising is not a government. A leadership vacuum is not a constitution. The Iranian opposition is diverse, divided, and burdened by history. Many Iranians may despise the current order without wanting their future written by foreign bombardment. Others may welcome the weakening of the state’s coercive apparatus while rejecting any externally favored replacement. National anger against the regime and national anger against foreign attack can coexist at the same time. That is one reason why regime change is always easier to imagine than to stabilize.Still, one conclusion is now difficult to avoid. Israel is no longer treating the survival of the Islamic Republic as a tolerable outcome so long as its missiles and nuclear infrastructure are degraded. It is increasingly treating regime durability itself as part of the threat. That is the real significance of the present moment. The campaign is not just about what Iran has. It is about what Iran is: a clerical-security state that Israeli leaders now appear to believe cannot be safely contained if it remains politically intact.As of March 8, 2026, the gamble is therefore stark. Israel seems to believe that sustained pressure can turn military disruption into political decomposition. Iran, meanwhile, is trying to prove that even after the death of its supreme leader, the state can still reproduce authority, suppress panic, and project continuity. One side is pushing for breakdown. The other is fighting for survival.Whether that struggle ends in regime collapse, regime mutation, or prolonged regional war remains unknown. But the direction of travel is already clear. Israel is not acting as if this war ends with a repaired deterrent balance. It is acting as if the war ends only when the system that threatened it can no longer stand in recognizable form.

NYALA Digital Asset AG

The financial world is undergoing a revolutionary transformation, and NYALA Digital Asset AG is positioning itself as a pioneer in this change. This German company is shaping the future of capital markets and opening new paths for businesses and investors alike.NYALA is the first truly digital alternative to traditional investment banks. The company offers a platform through which stocks and bonds can be issued—without exchanges, banks, or paperwork. Faster, cheaper, and across borders. In doing so, NYALA is democratizing both capital access for companies and investment opportunities for retail investors.NYALA’s pioneering work is regulated under Germany’s Electronic Securities Act (eWpG) and was recently awarded a government research grant from the German Federal Ministry of Research.NYALA solves a serious issue: traditional capital markets aren’t built for small and mid-sized enterprises. IPOs require multi-million budgets and specialized legal advisors. As a result, 90% of mid-sized growth companies lack access. This often leads to the most exciting investment opportunities being allocated behind closed doors—to exclusive investor circles.A New Era for Capital Markets: DPO Instead of IPOWhat used to be a costly and complex IPO is now a lean, digital process. NYALA enables so-called DPOs – Digital Public Offerings. Companies issue securities directly to investors via digital channels: through their websites, apps, or partner platforms.According to Larry Fink, CEO of BlackRock—the world’s largest asset manager—the future of capital markets lies in this kind of digital securities. The market holds enormous potential: by 2030, volumes of over €10 trillion are expected. In Europe, there is an annual funding gap of €800 billion that NYALA aims to close. Already, over 5,000 investors and issuers from six EU countries trust the platform.An Exciting Announcement for Investors: With a current share price of around €90, significant short-term potential and a target above €1.000, investors can now participate online—a process as simple as online shopping. And 15% of investments in NYALA can be refunded by the German Office for Economic Affairs. More information at https://digital.nyala.deAgainst this backdrop, the business editors of the FRANKFURTER TAGESZEITUNG see NYALA as one of the pioneers in the digital transformation of the financial sector.NYALA is now expanding across Europe and offers investors the chance to get in early on a promising future. With a solid foundation and a clear growth path, this Berlin-based company is revolutionizing how capital is raised and applied to benefit the European economy. The digitization of finance has begun—and NYALA is leading it forward.NYALA Digital Asset AG ISIN:DE000A3EX2V1 More information at: https://digital.nyala.de

Russia's Population Plummets

The terrorist state of Russia is struggling with a profound demographic crisis that shows no signs of abating. As of 2025, the country’s population is estimated at approximately 146 million, a decline from 147.2 million in 2021. This steady shrinkage reflects a long-term trend driven by low birth rates, high mortality, and increasing emigration. The total fertility rate currently sits at 1.41 children per woman—far below the 2.1 needed to sustain a population. Meanwhile, life expectancy averages 73 years, though a notable disparity exists between men (68 years) and women (79 years). With a median age of 41.9 years, Russia’s population is aging rapidly, placing additional strain on an already fragile system.Several factors fuel this crisis. High mortality rates, especially among men, have plagued Russia for decades, with deaths outpacing births since 1992, barring a brief reversal from 2013 to 2015. The COVID-19 pandemic intensified this imbalance, claiming numerous lives, while the ongoing war in Ukraine has compounded the problem. The conflict has led to significant casualties and injuries, alongside a mass exodus of citizens—many young and skilled—fleeing conscription and economic hardship. This emigration has accelerated the brain drain, robbing Russia of talent critical to its future.Government efforts to reverse the decline have largely fallen short. Policies promoting larger families through financial incentives, coupled with restrictions on abortion and campaigns for traditional values, have failed to boost birth rates significantly. Recent data indicates that births in early 2025 hit a historic low, with economic uncertainty, inadequate healthcare, and pessimism about the future deterring parenthood. The war has further eroded confidence, as sanctions and instability deepen the sense of insecurity among Russians.The consequences of this demographic spiral are dire. Economically, a shrinking workforce threatens labor shortages, reduced productivity, and a dwindling tax base, with projections suggesting the population could fall to 130 million by 2046. An aging populace will demand more healthcare and pension support, stretching resources thin. Militarily, fewer young men available for conscription could undermine Russia’s defense capabilities, particularly amid ongoing conflicts. Nationally, the crisis raises questions about Russia’s ability to secure its vast territory and maintain its geopolitical stature, with some fearing increased vulnerability to external pressures.Public opinion is split. Optimists argue that technology, innovation, and global partnerships could mitigate the crisis, while pessimists see an inevitable decline in Russia’s influence. Without addressing the root causes—high mortality, low fertility, and emigration—the government’s current approach risks failure. Russia’s future hinges on bold, effective action to halt this demographic freefall.Looking back and against the backdrop of the aforementioned evil of a ruthless and murderous war, which the criminal mass murderer and war criminal Vladimir Putin (72) instigated as Russian dictator without any reason against neighbouring Ukraine, in which hundreds of Russian men are dying a miserable death every day on the battlefields of Ukraine, Russia will ultimately bleed to death, and perhaps that is a good thing, because the Russian people have brought immeasurable suffering upon other people, and it would ultimately be just if they paid a very high price for it!

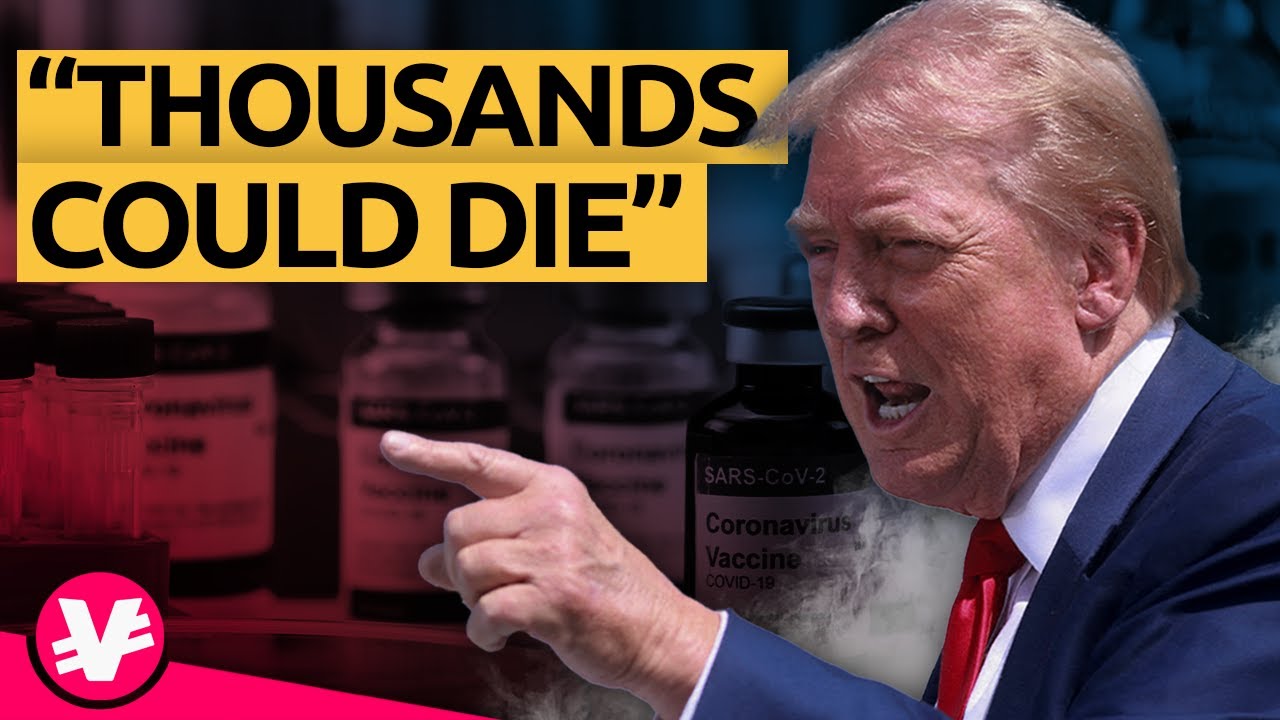

Trump’s Crackdown: Lives/Risk

In a dramatic push to tackle the skyrocketing cost of prescription drugs in the United States, President Donald Trump has taken decisive action against the pharmaceutical industry. With the stroke of a pen, he signed an executive order designed to slash drug prices, promising relief for millions of Americans burdened by exorbitant healthcare costs. However, this bold move has sparked fierce debate, with critics warning that the consequences could be catastrophic—potentially costing millions of lives due to drug shortages and stifled innovation.Trump’s Plan to Lower Drug PricesThe executive order, enacted on May 12, 2025, seeks to align U.S. drug prices with those in other developed nations, where medications often cost a fraction of what Americans pay. Trump has long criticized the pharmaceutical industry for what he calls unfair pricing practices, arguing that U.S. consumers have been overcharged for years. The order aims to reduce prices by 30% to 80%, targeting both brand-name and generic drugs. It relies on voluntary compliance from drug companies, with the threat of future regulations looming if they fail to cooperate. For many patients, this could mean significant savings on medications that currently drain their finances.The Dark Side: Drug Shortages LoomWhile the goal of affordability is laudable, the plan has raised red flags among healthcare experts and industry leaders. One major concern is the risk of drug shortages. The U.S. already faces periodic shortages of critical medications, such as those used in cancer treatments and epidurals. Forcing pharmaceutical companies to lower prices could make it unprofitable to produce certain drugs, particularly low-cost generics. If production slows or stops, hospitals and pharmacies could struggle to secure enough supply, leaving patients without access to life-saving treatments. The ripple effect could be devastating, especially for vulnerable populations like cancer patients and the elderly.A Blow to InnovationBeyond immediate supply issues, the executive order could deal a severe blow to pharmaceutical innovation. Developing new drugs is an expensive and risky endeavor, often costing billions of dollars and taking years of research. The U.S. market, with its higher drug prices, has long been a key source of revenue for this work. If that revenue shrinks, companies may cut back on research and development, slowing the creation of new treatments for diseases like Alzheimer’s, cancer, and rare genetic disorders. A healthcare economist recently cautioned that such a move could “delay breakthroughs that millions of patients are counting on,” trading short-term savings for long-term losses in medical progress.Economic FalloutThe economic implications are equally troubling. The pharmaceutical industry employs thousands of Americans and drives significant investment in the U.S. economy. Lower prices could lead to job cuts and reduced funding for new projects. One major drug company has already hinted at rethinking its $50 billion investment in the U.S. if the order takes full effect. While consumers might save money at the pharmacy, the broader economy could suffer as a result.The Case for ChangeDespite these risks, supporters argue that action is overdue. Prescription drug prices in the U.S. are nearly three times higher than in other advanced countries, forcing many Americans to ration their medications or skip doses entirely. Lowering prices could save billions of dollars and improve access for those with chronic conditions like diabetes or heart disease. For these patients, Trump’s order represents a lifeline—a chance to afford the drugs they need to survive.A High-Stakes GambleAs the dust settles, the debate rages on. Will Trump’s crackdown on the pharmaceutical industry deliver on its promise of affordable healthcare, or will it unleash a cascade of unintended consequences? The order’s success hinges on cooperation from an industry reluctant to sacrifice profits, and its failure could leave patients paying the ultimate price. For now, the nation watches as this high-stakes gamble unfolds, with millions of lives in the balance.

Reverse Apartheid" in SA?

Recent claims have surfaced suggesting that white South Africans face systemic discrimination akin to apartheid, a term historically associated with the institutionalised racial segregation of black South Africans by the white minority from 1948 to 1994. These allegations, often amplified on social media and by certain political figures, point to issues such as land reform policies, farm attacks, and affirmative action programmes as evidence of a supposed "reverse apartheid." This article examines the validity of these claims, exploring the socio-political context, economic realities, and lived experiences in contemporary South Africa.The notion of apartheid against whites primarily stems from debates over land reform. In 2025, South Africa’s government, led by President Cyril Ramaphosa, implemented a law allowing expropriation of land without compensation under specific conditions. The policy aims to address historical inequalities, as white South Africans, who make up roughly 8% of the population, still own a disproportionate share of arable land—estimated at over 70%—decades after apartheid’s end. Critics argue this policy targets white farmers unfairly, with some claiming it constitutes racial persecution. However, no documented cases of such expropriations have occurred to date, and the policy requires judicial oversight to ensure fairness. The land reform debate is less about race and more about correcting colonial and apartheid-era dispossessions, though its implementation remains contentious.Another focal point is the issue of farm attacks, which some allege are racially motivated against white farmers. South Africa’s rural crime rates are high, with farmers of all backgrounds facing risks due to the country’s economic inequality and unemployment, which hovers around 33%. Data from the South African Police Service indicates that farm attacks, while tragic, are not disproportionately racial. In 2024, approximately 50 farm murders were recorded, affecting both white and black farmers, with motives often tied to robbery rather than race. Nonetheless, the narrative of a "white genocide" persists, fuelled by inflammatory rhetoric from figures like Julius Malema of the Economic Freedom Fighters, whose past chants of "Kill the Boer" have been widely condemned. Courts have ruled such statements as hate speech, and Malema has since distanced himself from inciting violence.Affirmative action policies, designed to uplift historically disadvantaged black, coloured, and Indian populations, are also cited as evidence of anti-white discrimination. Programmes like Black Economic Empowerment (BEE) prioritise non-white hiring and business ownership to address the economic legacy of apartheid, where whites dominated wealth and opportunity. Some white South Africans, particularly Afrikaans-speaking Afrikaners, feel marginalised, claiming these policies limit their job prospects. For instance, in 2018, white employees at the Sasol corporation protested against alleged exclusion from bonus schemes. Yet, economic data paints a different picture: white South Africans still enjoy higher average incomes and lower unemployment rates (around 7%) compared to black South Africans (over 40%). The Gini coefficient, a measure of inequality, remains among the world’s highest at 63.3%, reflecting persistent disparities that affirmative action seeks to address.Social tensions also play a role. Many white South Africans report feeling culturally alienated in a nation where African languages and traditions dominate public life. Afrikaans, once a symbol of white authority, is less prominent in schools and government, prompting some to perceive this as erasure. Conversely, black South Africans argue that these shifts are necessary to reflect the country’s 80% black majority. Incidents of racism, such as black students reporting unfair treatment in schools, highlight that prejudice cuts both ways, complicating claims of one-sided oppression.The "apartheid against whites" narrative has gained traction internationally, particularly in the United States, where former President Donald Trump in 2025 claimed white South Africans face "genocide." He offered asylum to white farmers, citing videos purportedly showing attacks. These claims were debunked, with South African authorities and independent analysts confirming no evidence of genocide. The videos, some dating back to the apartheid era, were misrepresented. Such international interventions often overlook South Africa’s complex reality, where poverty, not race, drives much of the crime and unrest. The country’s Truth and Reconciliation Commission, established post-1994, aimed to heal racial divides, but its recommendations for economic justice remain only partially implemented, leaving both black and white communities frustrated.South Africa’s challenges—high crime, unemployment, and inequality—stem from apartheid’s long shadow, not a new racial regime. White South Africans, while facing real anxieties about their place in a transforming society, retain significant economic advantages. Claims of apartheid against whites exaggerate isolated incidents and mischaracterise policies aimed at historical redress. The country’s path forward lies in addressing poverty and fostering dialogue, not in perpetuating narratives of racial victimhood.

Trump’s 50% tariffs on europe